Download the Policybazaar app

to manage all your insurance needs.

Policybazaar offers complete paperwork and follow-up support to ensure quicker claim settlement with the insurer. We, at Policybazaar, simplify this by providing 100% dedicated claim assistance and ensuring nominees get guidance at every stage. Our dedicated claim assistance team provides end-to-end support from documentation and form submission to regular follow-ups with the insurance company. With us, you don't have to worry about the process; we simplify it for you, ensuring your loved ones receive the term insurance benefits smoothly and without unnecessary delays.

Share our claim helpline no.or claim card with your nominee

So that our friendly support team canassist your nominee in the time of need

Read moreWe assign a dedicated claim handler to your case once received

So that your family is not hassled by multiple calls and stakeholders

Read moreOur team takes care of all the details and document submission

(Death certificate, original policy documents, nominee details and KYC etc.)

Read moreWe represent your case to the insurer from day one — and escalate if needed.

We’ve even helped get rejected claims approved.

Read moreWe provide all these services free of cost, just so you can enjoy true peace of mind knowing that your family’s financial future is safe once you’ve bought a life insurance policy

We provide all these services free of cost, just so you can enjoy true peace of mind knowing that your family’s financial future is safe once you’ve bought a life insurance policy

Policybazaar Guarantees claim support for your family in those difficult times

₹3,017 Crore worth of claims settled since 2018

Policybazaar ensures your family gets what's rightfully theirs, even in your absence

The term insurance claim settlement process refers to the procedure through which the nominee receives the policy’s death benefit after the policyholder’s demise. It involves notifying the insurer, submitting the required documents such as the claim form and death certificate, and undergoing verification by the company. Once the claim is approved, the insurer releases the payout to the nominee’s bank account. This process ensures that the financial support promised under the policy is delivered to the family in a timely and transparent manner.

A term insurance claim should be filed immediately after the policyholder's death. While most insurers provide a reasonable time window, notifying them as early as possible helps avoid unnecessary delays.

Why filing early matters:

Quicker Settlement: Informing the insurer immediately allows them to begin processing your claim sooner, which helps ensure that the payout is released without unnecessary delays.

Fewer Issues: Delaying the claim notification can make it more difficult to collect documents or verify important details, which may slow down or complicate the claim process.

Meets Insurer Guidelines: Most insurance companies recommend that the nominee notify them within 30 days of the policyholder’s death to comply with claim filing guidelines and avoid any potential complications.

Only the appointed nominee, legal heir, or assignee (if applicable) can file the term insurance claim. Their name and relationship with the policyholder should match the records submitted during the policy purchase.

There are three types of term insurance claims:

Death Claim: This type of claim is filed when the policyholder passes away during the policy term. The nominee is required to inform the insurer and submit the necessary documents to receive the death benefit.

Rider Claim: If the term insurance policy includes add-on riders such as critical illness, accidental death, or disability cover, a rider claim can be raised when any of these covered events occur. The insurer then processes the claim as per the rider’s terms and conditions.

Maturity Benefit Claim (TROP): This claim applies only to Term Insurance with Return of Premium (TROP) plans. If the policyholder survives the entire term, they can claim the maturity benefit, which is the total premium amount paid, as per the policy’s provisions.

Our dedicated claims team helps verify and collect the required paperwork, making the process easier.

Call 1800-258-5881 or drop your name and contact number in the form above.

Our friendly support team is available 24×7. You’ll be assigned a dedicated Relationship Manager (RM) who will guide you through every step, making claim registration simple and stress-free.

Your RM will help you collect and verify the required documents:

(We can arrange free document pick-up at your doorstep)

Your dedicated RM will coordinate directly with the insurer — from submission to settlement.

We provide end-to-end support through their Claim Assistance Program. Here are the steps to file a claim through Policybazaar:

You can use the Claim Assistance Card to connect directly with your dedicated RM for help with the process. Also, it is advisable to formally notify Policybazaar by calling 1800-258-5881, emailing claims@policybazaar.com, or raising a request on the Claims section of the Policybazaar website or app. This ensures the claim process starts promptly and nothing is missed.

Provide key details, such as the policy number, policyholder's name, date of death, and cause of death.

Our team will guide you on the exact documents needed for your claim. In most cases, insurers allow you to upload scanned copies directly to their official claim portal or mobile app. If online submission isn't available, you can submit the physical copies at the nearest branch office of the insurer or hand them over to the claim settlement officer handling your case.

Policybazaar will coordinate with the insurance company on your behalf. The insurer will verify the documents, and if everything is in order, the claim is approved and processed.

Once approved, the claim amount is credited directly to the nominee's bank account. We will keep you informed at every stage until the settlement is completed.

Here is a list of the key documents required:

| Document | Where to Find / How to Get It |

| Original policy document | Available on your registered email, Policybazaar app under My Account (if purchased from PB), insurance company's app/website |

| Death certificate | Issued by the local municipal authority (Municipal Corporation/Council). Can be obtained online or in person by submitting the application and supporting documents |

| Valid photo ID and address proof of the nominee | Aadhaar card, Passport, Voter ID, Driving License, or any government-issued ID |

| Claim form (duly filled and signed) | Downloadable from the insurer's website or app; also available on the Policybazaar app. |

| Medical records (if applicable) | Collected from the hospital/doctor who treated the insured |

| FIR / Post-mortem report (in case of accidental or unnatural death) | Issued by the police station where the incident was reported and by the government hospital conducting the post-mortem |

| Bank account details of the nominee | Cancelled cheque or copy of bank passbook, available from your bank |

| Any other documents requested by the insurer | Shared directly by the insurer during claim processing |

We'll help you File Claim

If it hasn't been done already, we will immediately contact your insurer and file the claim on your behalf.

We Give End-to-End Support

Your dedicated claim manager guides you through every step, handling all documentation and formalities.

We'll Keep Follow-Up on Your Behalf

We stay in touch with the insurer to push for quick verification and settlement.

We Won't Give Up

If your life insurance claim is unfairly rejected, we escalate it to the insurer's grievance cell for resolution.

We'll Fight for You

If needed, we help you approach the Insurance Ombudsman and represent your case until it's resolved.

Contact our claim assistance team directly if your nominee has to make a claim.

Contact us at 1800-258-5881

Email claims@policybazaar.com

Filing your term insurance claim through Policybazaar offers several advantages:

24X7 Claims Support: At Policybazaar, our relationship with you doesn't end when you buy a policy; it begins there. In moments of urgency, our trained and responsive support team is just a call away, ready to guide you with speed and care 24/7 (all days). No endless queues, no piles of paperwork, just quick solutions and heartfelt assistance you can count on every time.

Claim Assistance Card: Whenever you buy a term plan from Policybazaar, you receive a Claim Assistance Card that can be shared with your nominee. This card helps ensure a hassle-free claim settlement when the time comes. It includes important details such as the policy name and number, the life assured's name, the sum assured, and the date of birth. It also carries the Relationship Manager's contact information (name, phone number, and email) for quick and easy support.

Direct co-ordination with insurers: At Policybazaar, our representatives work closely with leading insurance companies to ensure your family's claim settlement process is simple, smooth, and hassle-free. We assist in understanding complex documents, help with form filling, address claim-related queries, and coordinate directly with the insurer to ensure the claim is processed as quickly as possible.

Complete Document Assistance: We help collect, verify, and submit all required paperwork.

Real-Time Claim Tracking: We provide regular updates on progress via SMS, email, and phone so you're never in the dark.

Zero Cost Service: Claim assistance is free for all term insurance policies purchased through Policybazaar.

To ensure a hassle-free experience, here are a few mistakes you should avoid:

Delaying the claim intimation

Submitting incomplete or incorrect documents

Not disclosing accurate information

Ignoring follow-up emails or calls from the insurer

Providing the wrong bank account details

We help avoid such errors by reviewing and validating all documents before forwarding them to the insurer.

Filing a term insurance claim may feel overwhelming during a difficult time. However, with Policybazaar's dedicated support, the process becomes much more manageable. The team ensures that nominees receive timely guidance, help with paperwork, and updates until the claim is settled.

If your term insurance policy was purchased through Policybazaar, you are entitled to free, dedicated claim assistance. All you need to do is raise a request, and out team will take care of the rest, professionally, promptly, and with empathy.

Note: You should also check the benefits of term insurance if you are planning to purchase the term insurance plan.

Claim assistance card

We will provide a Claim Assistance Card for your nominee to ensure they have handy policy details as well as direct claims assistance number always with them.

Personal Claim Handler

A dedicated claim expert will be assigned to your family to guide them through the entire claims process — from start to finish.

Step by step free documents pick-up

We will keep your family posted at every stage of claim processing. We help your family navigate through complicated documents and emails & provide pick-up facility at doorstep.

Required Documents: Death Certificate: Original death certificate and an attested copy issued by the local municipal authority.

Insurance Policy: Policy documents issued by Policybazaar or the insurance company.

Medical Records: Admission form, discharge report/summary, test reports, etc.

Bank account details: Nominee's account details in which claim amount would be credited.

Nominee details: Name, date of birth, relationship with the insured, and other relevant details.

Customer Story

Claim Initially Rejected. Settled with Policybazaar’s Help. Policybazaar’s free claims assistance ensured Mr. Gangurde’s family received the full amount—supporting them emotionally & financially when they needed it most.

The Late Mr. Vivek Vijay Gangurde, a self-employed businessman from Nashik, Maharashtra, purchased a Term insurance plan on 29th June 2022, hoping that his family would never require assistance from it in the future. Tragically, severe jaundice claimed his life on 05th March 2024.

This tragic event deeply affected the entire family, both emotionally and financially, as the late Mr. Gangurde was vital to their family business. On March 6, 2024, Mr. Aniket Vijay Gangurde, the brother of the insured, reached out to policybazaar.com to inquire about the claims process. Given the difficult circumstances, he emphasized the need for a quick settlement of the claim to support his family’s immediate needs. The Policybazaar team guided him diligently through each step, reassuring him that they would manage the claim until a resolution was achieved. However, during the claim investigation, the insurance company highlighted a discrepancy in the proposal form. This finding left the family devastated, and they requested assistance from the Policybazaar claims team to have their claim reconsidered. The team diligently investigated the case and identified key points that needed to be addressed with the insurance company. Fortunately, Policybazaar team was able to address the discrepancy as highlighted by the insurer and presented the case to the insurer’s claims review committee and senior officials, urging them to reconsider the claim. Ultimately, the insurer was persuaded by the appeal, and the Policybazaar team successfully secured the full claim amount, which was deposited into the nominee's account on April 2, 2025.

The family expressed their gratitude for the Policybazaar team’s commitment to going the extra mile in their time of need. They particularly appreciated the free claims assistance provided by the Policybazaar.com claims team, who supported them like a family member during an especially difficult period marked by mental, financial, and emotional challenges.

˜The insurers/plans mentioned are arranged in order of highest to lowest Sum Assured(SA) offered by Policybazaar’s insurer partners offering term insurance plans on our platform, as per ‘first year premium of life insurers as at 31.03.2025 report’ published by IRDAI.Policybazaar does not endorse, rate or recommend any particular insurer or insurance product offered by any insurer. For complete list of insurers in India refer to the IRDAI website www.irdai.gov.in

˜Policybazaar Promise reflects the guarantee offered by insurers. Price assurance is based on certifications shared by insurers with us.

+On the basis of your profile

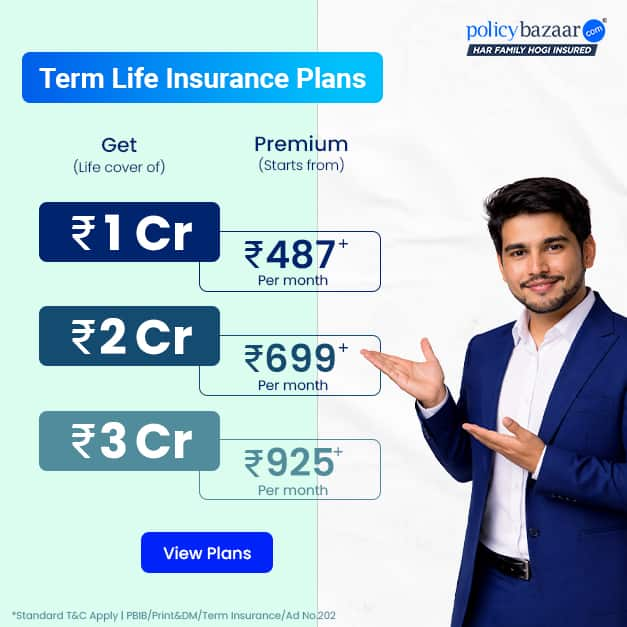

+Rs. 410/month is starting price for a 1 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10

+Rs. 410/month (Rs.14/day) is starting price for a 1 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age rounded off to nearest 10

+Rs. 245 is starting price for a 50 lakhs term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 8/day is starting price for a 50 lakhs term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10

+Rs. 15/day is starting price for a 75 lakhs term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10

+Rs. 504/month is starting price for a 1.5 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 494/month is starting price for a 2 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 636/month is starting price for a 3 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 918/month is starting price for a 5 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 1,286/month is starting price for a 7 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 453/month is starting price for a 1 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs.582/month is starting price for a 2 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 786/month is starting price for a 3 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 1,374/month is starting price for a 5 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 1,592/month is starting price for a 7 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 525/month is the starting price for a 1 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 68 years of age.

+Rs. 668/month is starting price for a 2 crore term life insurance for an 25 year-old male, non-smoker, with no pre-existing diseases, cover upto 45 years of age.

+Rs. 1,200/month is starting price for a 2 crore term life insurance for an 35 year-old male, non-smoker, with no pre-existing diseases, cover upto 55 years of age.

+Rs. 410/month is starting price for a 1 crore term life insurance for an 18 year-old Female, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 577/month is starting price for a 1 crore term life insurance for an 18 year-old Male, self employed, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

*The full refund of premium is available on availing the one-time option of refund of premium. Total premium paid for policy (paid for add-ons) will be the special exit value, payable on availing the one-time option of refund of premium if you wish to completely exit the policy.

+Rs. ₹361/month is the starting price for a ₹1 crore loan cover with an 8% interest rate for an 18-year-old male, non-smoker, with no pre-existing diseases, loan tenure up to 20 years, rounded off to the nearest 10

Prices offered by the insurer are as per the IRDAI approved insurance plans | #All savings and online discounts are provided by insurers as per IRDAI approved insurance plans | Standard Terms and Conditions Apply | **Tax Benefits are subject to changes in tax laws.| Policybazaar Insurance Brokers Private Limited

We will respond in the first instance within 30 minutes of the customers contacting us. 30-minute claim support service is for the purpose of giving reasonable assistance to the policyholder in pursuance of the claim. Settlement of claim (including cashless claim) is the responsibility of the insurer as per policy terms and conditions. The 30-minute claim support is subject to our operations not being impacted by a system failure or force majeure event or for reasons beyond our control. For further details, 24x7 Claims Support Helpline can be reached out at 1800-258-5881

For more details on risk factors, terms and conditions, please read the sales brochure carefully before concluding a sale

Policybazaar Insurance Brokers Private Limited | CIN: U74999HR2014PTC0534

© Copyright 2008-2026 policybazaar.com. All Rights Reserved

Tata AIA Life Insurance has launched a student-focused term

Read more

Home loan interest rates in West Bengal typically range between

Read more

A home loan is a secured loan used to purchase, construct, or

Read more

The Ageas Federal Life Insurance Super Protect Plus Plan is a

Read more

Emergency management is the systematic approach to planning for

Read moreInsurance

Calculators

Payment Methods

Secured With

Follow us on