Download the Policybazaar app

to manage all your insurance needs.

One of the popular and traditional schemes that Indian post offices have been offering for years is the saving schemes. Many Indian households still prefer putting their hard earned money in a Post Office fixed deposit scheme as it is backed by the Government of India. Also, people who do not have a bank in their vicinity can invest in the nearest Post offices as well.

Includes life cover

Includes life cover

Completely Tax free^

Completely Tax free^

People in rural areas invest more in post office deposits in comparison to bank deposits. Nowadays the government allows private banks and public sector banks to open a post office fixed deposit scheme for its customers.

A fixed deposit is an investment scheme that allows one to deposit in fixed deposits in order to earn interest on the investment. The duration of these FD is 1-year, 2-years, 3-years and 5-years. The fixed deposit interest rate currently varies from 6.9% to 7.7%. The FD interest that is paid is charged with Tax Deduction at Source (TDS). By investing in this deposit scheme one can get tax benefits under section 80C in the old tax regime.

The FD scheme or post office time deposit makes a good alternative to the bank FD. Indian Postal Services enable an individual investor to invest money in a post office fixed deposit scheme and earn a guaranteed return on the deposited amount for a fixed span of time.

The account can be opened by:

A single adult

Minor above 10 years of age

Joint Account (3 adults max.)

A guardian on behalf of a minor/ or specially challenged person

Post office savings account holders with internet banking facility can open FD or Post Office time deposit (POTD) scheme online.

A post office fixed deposit scheme is suitable for conservative investors like retirees or those about to get retired. It makes an ideal investment option for those who are looking for a low-risk investment option with a steady income along with capital protection.

Both cash and cheque payments can be done to open a post office fixed deposit scheme. If the payment is done via cheque then the date of realization of the cheque shall be considered as the date of opening the account. However, NRIs cannot open a post office fixed deposit scheme.

From premature withdrawals to the integration of savings account or integration with recurring deposits, there are various features and advantages that follow. Some of them are discussed below:

Fixed Deposit Investment Amount – There is no limit on the number of accounts in a post office. However, there can be only one deposit for one specific amount. The minimum deposit limit is Rs. 1-00 with no limit on the maximum amount (in multiples of Rs. 100 only).

FD Maturity – Once the scheme is matured, a renewal form needs to be filled. However, some post offices with CBS facilities provide the auto-renewal option as well.

Integration with RDs– The account holder can file an application to direct the monthly interest payments to a five year RD. Provided the savings account is in the same post office. This facility is available only at the HOD sub- Post offices.

Integration the Post Office Account with the Savings Account – The account holder can also instruct the post office to redirect the FD interest earned to the savings account in the same post office. This facility is also available only at the HOD sub- Post offices.

Premature withdrawal – Premature withdrawals on the post office fixed deposit scheme is not allowed before six months. If one exits within 6 months to 1 year then the interest earned will be reduced to 4%. After that, the account holder can exit with a 1% penalty on the FD interest rate.

Taxation – The tax benefits under section 80C are valid only on 5-year FD. FDs with tenure of less than 5 years are not eligible for tax benefits. The interest earned on such FDs needs is taxable as per the applicable tax rate.

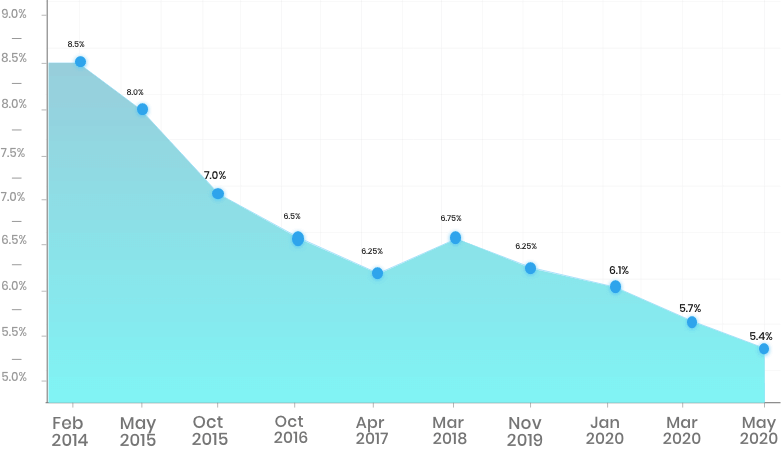

The government decides the FD interest rate that is paid every year but is calculated quarterly. The FD interest rates for January 2020 to March 2020 remain the same as in the previous quarter and are given in the table below:

| Scheme | Post Office Fixed Deposit Interest Rate (in %) |

| 1-year | 6.9 |

| 2-years | 6.9 |

| 3-years | 6.9 |

| 5-years | 7.7 |

*Trad plans with a premium above 5 lakhs would be taxed as per applicable tax slabs post 31st march 2023

All savings are provided by the insurer as per the IRDAI approved insurance plan. Standard T&C Apply

A FD calculator makes a great investment tool to calculate the returns on FDs:

The calculator breaks up the maturity value into interest earned and the maturity value.

Information required for the calculator includes:

Investment Amount

The current rate of FD interest

Investment tenure

Deposit Term

Frequency

And then click calculate

For instance, if the invested amount is Rs.1 lakh for a period of 5 years in a FD, the total interest earned will be Rs.46, 034 and the maturity value of the deposit will be Rs.1, 46,034.

You May Also Like: Post Office Interest Rate

Once the post office branch is selected to open the time deposit account, the following documents are required:

The applicant needs to fill and submit the FD opening form.

Address and ID Proof such as the Aadhaar card or passport copy.

Declaration in Form 60 or 61 or PAN (permanent account number) card.

Voter's ID, driving license, or ration card.

Original ID proof is required for account verification.

Mention a nominee and get the signature of a witness to complete the formalities.

28 Mar 2025

A Public Provident Fund (PPF) account with the Bank of India is

27 Mar 2025

The Swatantra Yuva Udyami Scheme (SWAYAM), launched by theInsurance

Calculators

Payment Methods

Secured With

Follow us on