Download the Policybazaar app

to manage all your insurance needs.

Fixed Deposits are a sum of money deposited for a specific period in a bank account. And in return, you get interested in the principal amount when the tenure matures. The IDBI Bank FD calculator is an online tool that helps calculate the amount of money received as a return at the end of maturity. It is mandatory to provide PAN card details to start a Fixed Deposit account.

Guaranteed Plan

(By Insurance companies)Fixed Deposit

(Offered by Banks)Savings Account

(Post Office)

Fully Tax-Free, Life Cover Included

Using these just needs to give a few details to know the return amount on the deposit. The details might include the principal amount, tenure period, and he/she should be aware of the interest rates offered. It is calculated using a formula:

A=P (1+r/n)^n*t

A-Maturity amount

P-Principal amount or sum of investment

R-Interest rate per year

N-Number of times the interest applied is compounded

T-Maturity period

IDBI Fixed Deposit calculator uses the same formula, but it saves time using this, and there is little scope of error in calculation.

Many factors affect the returns on an amount deposited:

Term of investment-Choosing the correct maturity term is significant to yield more interest. IDBI Fixed Deposits are beneficial both short-term and long-term, but since the compound rate of interest calculation is applied here; it is more beneficial for long-term investments.

Principal amount -If the amount invested is maximized, it can achieve more returns.

Interest rate-If the principal amount and tenure period are kept constant; the interest rate will determine the return amount. The more the interest rate, the more will be the return amount. IDBI Bank FD Calculator helps compare different interest rates.

Interest Compounding Frequency-This is the frequency at which interest is compounded. It can be monthly, quarterly, half-yearly, or yearly. The more the compounding frequency, the more the investor earns on the deposit.

TDS Applicability and TDS Rate-(Tax Deducted at Source) is how the bank deducts from the interest income and remits it to the central government. It is set at an average of 10%.

With simple interest, the interest is only earned on the principal amount, whereas with compound interest, the interest is earned on the principal and the interest.

Simple interest is calculated by the formula:

SI= (P*r*t)/100

Where:

P- Principal amount

r- Rate of interest

t- Time period

In compound interest, you earn interest on the principal amount, and you earn interest in interest. But one should make sure the interest rate is reasonable and see how many times interest will apply on interest in a year; that is, the number of times interest is compounded.

Compound interest is calculated by:

For example, the bank offers 8% per annum for a five-year deposit, and the interest is compounded annually. And if the amount invested is Rs. 10,000

Year 1

10,000*8*1/100=Rs.800

This is added to the principal amount, which makes it Rs.10, 800.

Year 2

You will earn interest on Rs.10, 800

10,800*8*1/100=Rs.864

This is again added back, which makes it Rs.11, 644.

The formula is:

CI=P {(1+i/100)n-1}

Where P-Principal amount

N-Number of years

I-Interest rate

*Trad plans with a premium above 5 lakhs would be taxed as per applicable tax slabs post 31st march 2023

All savings are provided by the insurer as per the IRDAI approved insurance plan. Standard T&C Apply

Plan smarter with our SIP Calculator.

One has to enter a few basic details, and the calculator does the job.

There are a few other factors that might affect the rate of interest that is beyond the control of the investor.

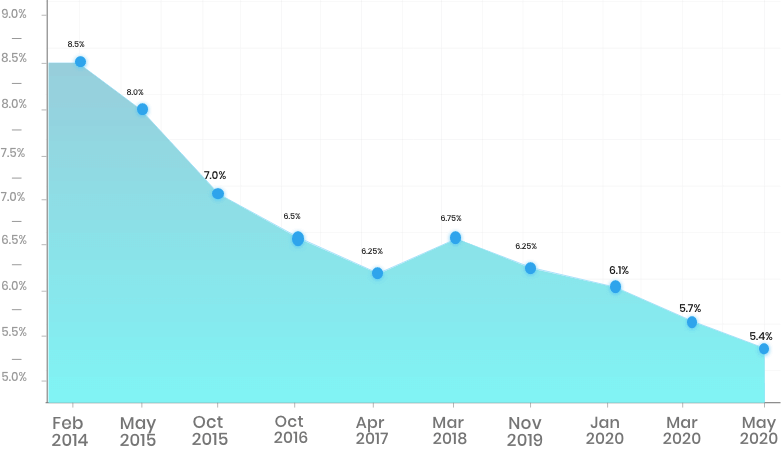

IDBI Bank is one of the leading financial institutions in the country, and their fixed deposits are one of the most convenient means to deposit your excess funds and generate interest. However, the consumer needs to be aware of the interest rates offered by the bank. It is different for general citizens and senior citizens. They offer an interest rate of 5.10% for general citizens and 5.60% for senior citizens over one year. Senior citizens are given an extra 0.5% interest per year. The IDBI FD calculator helps calculate the interest that will be generated even before investing. What should be kept in mind is to check the table of interest rates with the bank. Fixed deposits are all about minimizing risk and guaranteed returns.

In a Nutshell

With the use of the IDBI FD calculator, one can determine the profit they can earn on a given investment and calculate how much they should invest in getting a particular amount and in how much time they will receive that. If one wants to double the funds, this calculator will give the period to double the funds. It will calculate the tax deductions also and give the desired result. Since a Fixed Deposit is a safe investment, it is even better to go for it with premeditated calculations, thus eliminating all risks.

A1. Yes, it is possible to withdraw your money before the maturity period is completed, but it might affect the returns. Moreover, there is a one-year lock-in period where no withdrawal is possible.

After this, the premature withdrawal charges may apply, which will be the average benchmark rate of the immediately preceding quarter with the markup of the applicable preceding term.

A2. You can open an account with a mere Rs. 10,000. There is no upper limit in investing in IDBI Fixed Deposit.

A3. This is calculated using the rule of 72. One needs to know the interest rate for this. Considering the interest rate to be 6.95%, divide 72 by the interest rate. So, in this case, 72/ 6.95= 10.36

So it will take a little over 11 to 14 years for the amount to double, considering the 10% tax deduction.

A4. The minimum term of the deposit is 15 days, and the maximum is up to 20 years. However, it is advisable to opt for long-term investment considering the compounding of interest rates.

A5. A guardian can open a joint account with the minor on his/her behalf. The minor will receive the earning of the FD once he is 18 years or whenever the FD matures (whichever comes earlier). Till that time, the guardian remains in charge of the account.

A6. Yes, it is possible. It is a secured loan that you take by pledging the fixed deposit as the collateral. You don't have to break the Fixed Deposit to take a loan against it. No credit score check is required to take a loan against Fixed Deposit. All Fixed Deposit holders, including joint account holders, can apply. Minors are not eligible to apply for this. Investors of a 5-year tax-saving FD cannot apply for this. Loans are offered at a lower interest rate.

A7. Yes, it is. As per the Income Tax Act, when the interest earned in the financial year exceeds Rs.40, 000, Tax Deductible Source is applicable on the credited interest.

However, one can claim tax deductions up to Rs.1.5 lakh per financial year. There are tax-saving FD schemes also available. But it does not apply to senior citizens since the interest rate is already high.

03 Sep 2021

Fixed deposit schemes are a popular investment instrument due to

14 Jul 2021

A Monthly Payout FD Calculator is a special online calculatorInsurance

Calculators

Payment Methods

Secured With

Follow us on